Products You May Like

Were you unable to attend Transform 2022? Check out all of the summit sessions in our on-demand library now! Watch here.

In the wake of COVID-19, it became apparent to investors that the megalithic supply chain monopoly they were working with — China — has its limits. Relying on a single faraway source to manufacture and distribute practically everything in our vital electronics market began to feel risky, and companies increasingly sought ways to make their supply chains more resilient and diversified. Investors are looking seriously at India as an alternate supply chain as part of this massive decision — and one that is not being made simply based on trade wars.

It needs to be seen whether India is a reasonable risk for global electronics companies looking to relocate to a new electronics manufacturing hub.

Historically, the business environment in India has not been very conducive to these kinds of initiatives. In purely economic terms, global players choose to work in areas that are simpler and easier; in the last decade, India has not been characterized by a stable government that is purely focused on investments. However, this has begun to change in the last five or six years and seems unlikely to revert any time soon. Let’s take a look at some of the changes wrought by recent developments in policy in India’s early-stage transformation.

By 2016, India was the fifth largest manufacturer globally, with a total Manufacturing Value Added (MVA) of over $420 billion. Manufacturing in India has grown at 7% annually and constitutes 16 to 20% of its total GDP. With its fast-growing economy and population of 1.4 billion people — making it the second largest and demographically the youngest country in the world — India has almost unprecedented consumer demand, and with it, growing demand for manufacturing on home soil.

To that end, there are several sectors, including automotive manufacturing, in which India is already self-sufficient. Almost all car brands in India sell vehicles that are made, assembled, and sold in India. In terms of demand, Indians have an insatiable appetite for two things: gold and electronics — and particularly in electronics, they want the latest and greatest. As a result, you’ll find more electronics brands in India than in the U.S. — India hosts American, German, Korean, Chinese, even Turkish brands. But to get to even a fraction of the scale of China, India will need to become a hub for manufacturing and exporting electronics globally.

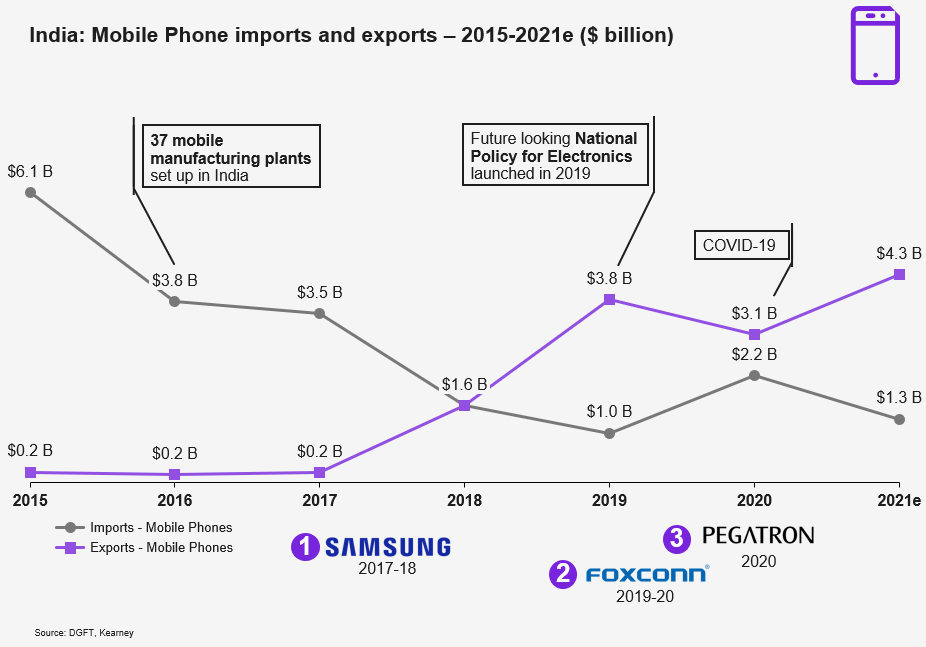

A success story: mobile phones

In the last six years, the Indian government has actively sought to bring in foreign investment and grow the country’s manufacturing economy. With the 2014 “Make in India” initiative and a 2017 infrastructure stimulus toward building a more connected economy, they focused first on the most critical areas to the Indian market — mobile phones and TVs. As a result, they created incentives for those two industries at national and state levels.

And major phone manufacturers responded — they asked how they could create an ecosystem and where the most applicable market was. Since most Indians’ introduction to the internet is on their mobile phone, with the cheapest data costs in the world — India seemed like the answer.

So, the Indian government picked up this horse and bet their house on it, determined to make it a success. They persuaded Samsung and Apple to manufacture phones in India. The initial consumption was massive— within two years, 100% of phones made in India were used in India, resulting in lower imports. Since then, Apple and Samsung have started to export out of India, to the extent of 70-100 million phones over the last couple of years. In fact, Samsung is continuously improving its production capacity in India to reach 29% of global production by the end of 2022. The question now is, can this trajectory be replicated in other electronics subsectors?

Not as easily, it turns out. While the jury is still out on television manufacturing, India has been less successful with laptops and computers. There are structural issues that make it not as quick a win as the phone story, but the roadmap is the same: a significant core company needs to set up shop in India to become an alternate, complete electronics ecosystem. But not just any company: an Intel, a Micron, a Western Digital, a Seagate — if one of these sets up shop in India, the rest will follow. If any of these players come, their component manufacturers will set up in India too, and all the tiny but necessary little parts will come with them.

India’s grand ambitions are backed by strong policy push and fast forward speed

India aims to produce $300 billion worth of electronics by 2026, a ~3.5 times increase than its 2021 production. To enable this growth, India is actively engaging with industry players. It has refined/launched subsidies worth ~$10 billion for companies looking to establish/expand semiconductor fabrication (fab), display fab, compound semiconductor fab, and packaging in India.

This is over and above existing initiatives such as Production Linked Incentive (PLI) Scheme, which has greatly benefited the mobile industry. Along with favorable subsidies, the Indian government is vocal about faster business application processing turnaround and stability in import tariffs.

Setting up India Semiconductor Mission (ISM) — a specialized business unit focused on building semiconductor and display ecosystems — drafting and approving strong subsidies for semiconductor fab, and ecosystem are some steps the government has taken to demonstrate its commitment.

In our fire chat with Saurabh Guar, joint secretary (electronics), ministry of electronics & IT, he mentioned that the recently announced ~$10 billion Semicon India Programme has seen considerable interest from the semiconductor industry. Despite aggressive timelines for submission, the ISM has received five applications for semiconductor and display fabs with a total investment to the tune of $20.5 billion (INR 153,750 Crore). We expect India to become an internationally conductive and competitive destination for semiconductor and display manufacturing.

The electronics ecosystem: What is missing?

To understand where India is now and where it wants to be, it’s helpful first to break down the capabilities needed to manufacture electronics. Unlike food or auto manufacturing, electronics is not homogeneous — it requires three distinct capabilities.

What we see as the final product, the “box,” results from the final assembly process — a capability that is already as high in India as it needs to be. While India does this handily, and some Indian companies have been doing electronics manufacturing at this level for upwards of 30 years — they haven’t reached a point where they could export to the world or compete with the big powers in Southeast Asia and China.

Critically, final assembly accounts for about 10 to 20% of the value in the electronics ecosystem; the other 80 to 90%, which needs to be imported into India, consists of the other two capabilities — the raw material or components and the submodules or subassemblies. India will need to acquire these to become a complete manufacturing hub. So, let’s look at these two areas a little more closely.

The submodule level — which includes, for example, displays for TV or phone — constitutes a product category unto itself. These products require a complex manufacturing process, with multiple layers and intricate electronics — that’s how the module works. This capability doesn’t yet exist in India; it remains a keen governmental focus to get it there.

The components are broken down into three main categories: actives, passives, and interconnects or electromechanical connectors. Of these, 60 to 80% of the money is in the actives, including microprocessors, memory, storage, GPUs, ancillary chips, power management chips, etc. None of this is manufactured in India right now; China is also trying to acquire this capability. To do so would require a semiconductor fabrication plant costing $8 billion or more.

A handful of companies control this space — Intel, TSMC, GlobalFoundries, Infineon Renaissance, TI — and to acquire this critical capability would mean convincing one of them to have a presence in India.

Next, come the passives — the nuts and bolts of electronics. Without them, you can’t make a product —inductors, resistors, capacitors, etc. Finally, the electro mechanicals — motors, wire harnesses, connectors —can also be pretty expensive. To some extent, these are manufactured in India, but there’s still a gap that needs to be closed. To obtain a sustainable ecosystem, India will have to draw these manufacturers either within its geographic boundaries or within its own sphere of influence.

Right now, only 10 to 20% of the value in the electronics market is in India, while 80 to 90% needs to be imported. This gap won’t bridge right away — while the passives can be managed easily, computers, memory, and storage will pose a more significant challenge. Consider that it can only be done by one of the three memory players in the world — Samsung, Micron, and SK Hynix — or just a handful of mainstream processor manufacturers — Intel, TSMC, Samsung and Global Foundries.

India vs. Southeast Asia

It takes time to change over ecosystems — indeed, it’s taken China more than three decades to build the capacity they now have — and while India is working on getting its capabilities in place, other attractive alternatives are emerging. Vietnam is one such country; Thailand, Indonesia, and Cebu in the Philippines have all become attractive hubs for investment. Of course, if you need a labor pool of 20,000 people, Cebu can’t give you that, while India can; but initially, as companies are experimenting, they won’t need that many people to try something out. However, once a certain scale and size is reached, the decision will come down to the sheer availability of talent.

Not many countries have the capacity to become a second factory (after China) for the world. In this sense, India’s strength lies in its sheer numbers — in all likelihood, it will become the world’s most populous country very soon. Its young demographic comes with a sharp focus on STEM education and vocational training. Additionally, labor rates are among the cheapest on the planet, alongside Vietnam’s. Indians have a concept, jugaad, which roughly translated means a flexible approach to problem solving — there is a national instinct to figure out ways to do things in innovative and cost-effective ways.

This is what India brings to the table, beyond the mass of demand. The raw material is in place for India to become the secondary ecosystem for the electronics supply chain — but it will take at least three to five years to get there.

Structural challenges to India becoming a manufacturing hub

While India is rich in human capital, it doesn’t yet have the infrastructure to create the entire ecosystem. As a democracy, India makes decisions and takes action more slowly. Sustainable resources pose another challenge — India needs to diversify its energy sources and reduce emissions. The labor force is relatively young. While it is growing fast, it will need upgraded education curricula, revamped vocational training, and programs to improve digital skills to bring the workforce up to speed.

Of course, its greatest challenge is China. How can India begin to compare itself with China, especially regarding electronics hardware? What can India realistically take over, and what is firmly entrenched in China? Consider that, for human-interacting devices, there has to be a display — and the vast majority of these are made in China and Korea. Korea manufactures some displays with Samsung and LG, and some display manufacturing/assembly has begun to spring up in India, but the biggest companies are still in China.

There are no semiconductor fabricators in India, and China has long had a near-monopoly on printed circuit boards — India is just starting to manufacture these. The entire ecosystem for passive parts is in China and Taiwan.

On how many of these levels could India compete? Many different categories of components are single-threaded in China and very difficult to replicate elsewhere. The finished goods market is reasonably diversified, but as we’ve discussed, it’s a tiny proportion of the product’s value. We estimate that 60% of sub-assemblies worldwide come from China — this capability is easier to move out but will require a knowledgeable workforce. The raw components will be the hardest of all to relocate — even if the design is done in Taiwan or Japan, most raw component manufacturing comes from China.

The diversification of component supply to places like India is just starting. India has been making subassemblies and finished goods for a long time — Nokia had a plant in India for 15 years — but what has been missing is the component supply chain. Setting this up in India is more of a journey, though it is now at a critical scale.

We started and will end with COVID: Will the need for resilient supply chains permanently affect the electronics manufacturing industry? Some feel that these setbacks will play favorably in the Indian market, but there remains a long and defined path before India can challenge the electronics giant.

Bharat Kapoor is lead partner for Hi-Tech in global strategy and management consultant for Kearney’s Communication Media & Technology practice.

DataDecisionMakers

Welcome to the VentureBeat community!

DataDecisionMakers is where experts, including the technical people doing data work, can share data-related insights and innovation.

If you want to read about cutting-edge ideas and up-to-date information, best practices, and the future of data and data tech, join us at DataDecisionMakers.

You might even consider contributing an article of your own!